Know how life insurance works, policy types, coverage options, and rates in 2026. Compare term, whole, and final expense plans easily.

Key Takeaways

- Life insurance provides financial protection for your family through a tax-free death benefit.

- Term life insurance is usually the cheapest and most popular option.

- Rates vary widely by age, health, lifestyle, and policy type.

- Major insurers offer multiple life insurance policies with flexible coverage amounts.

- Understanding policy riders, claims, and coverage types helps you choose confidently.

Life Insurance Guide 2026 — What You Need to Know Before You Buy

Life insurance is one of the most important financial tools for protecting your family’s future. If you were no longer around tomorrow, a life insurance policy provides a tax-free payout your loved ones can use for daily living expenses, funeral costs, mortgage payments, debt payoff, and long-term stability.

What Is Life Insurance and How Does It Work?

Life insurance is a contract between you and an insurer. You pay monthly or yearly premiums, and in exchange, your beneficiaries receive a lump-sum payment (called the death benefit) after you pass away.

Common Uses of the Death Benefit

- Funeral and medical costs

- Mortgage payoff

- Replacing lost income

- College expenses

- Debt repayment

- Long-term family support

Disclosure: Prices vary by age, state, health, and provider.

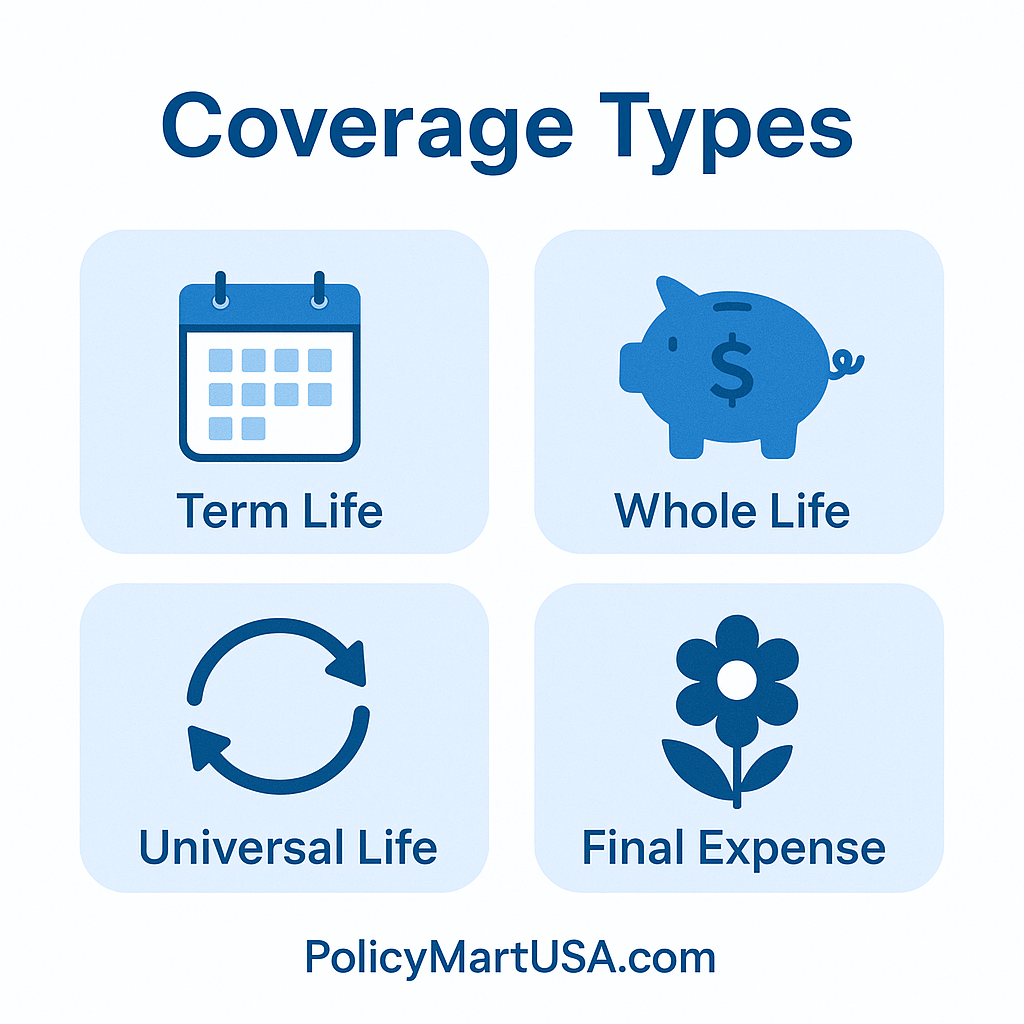

Types of Life Insurance Policies

Life insurance policies generally fall into two categories: term and permanent.

1. Term Life Insurance (Most Popular & Affordable)

Term life provides coverage for a set period—usually 10, 20, or 30 years. If you pass away during this period, your family receives the benefit.

Best For:

- Young families

- Income replacement

- Budget-friendly protection

Pros:

✔ Lowest rates

✔ Simple structure

✔ Can convert to permanent in many cases

Cons:

✘ No cash value

✘ Coverage ends after the selected term

2. Whole Life Insurance (Lifetime Coverage + Cash Value)

Whole life insurance lasts your entire life as long as premiums are paid.

Features:

- Guaranteed death benefit

- Cash value that grows at a fixed interest rate

- Level premiums

Best For:

- Estate planning

- Long-term financial needs

- People wanting cash value accumulation

3. Universal Life Insurance (Flexible Permanent Coverage)

Universal life lets you adjust your premiums and death benefit over time.

Sub-types include:

- Indexed Universal Life (IUL)

- Variable Universal Life (VUL)

These policies offer flexible cash value growth tied either to market performance or fixed rates.

4. Final Expense Insurance (For End-of-Life Costs)

Designed to cover:

- Funeral expenses

- Medical bills

- Legal costs

No medical exam is usually required.

Get Your Free Insurance Quote

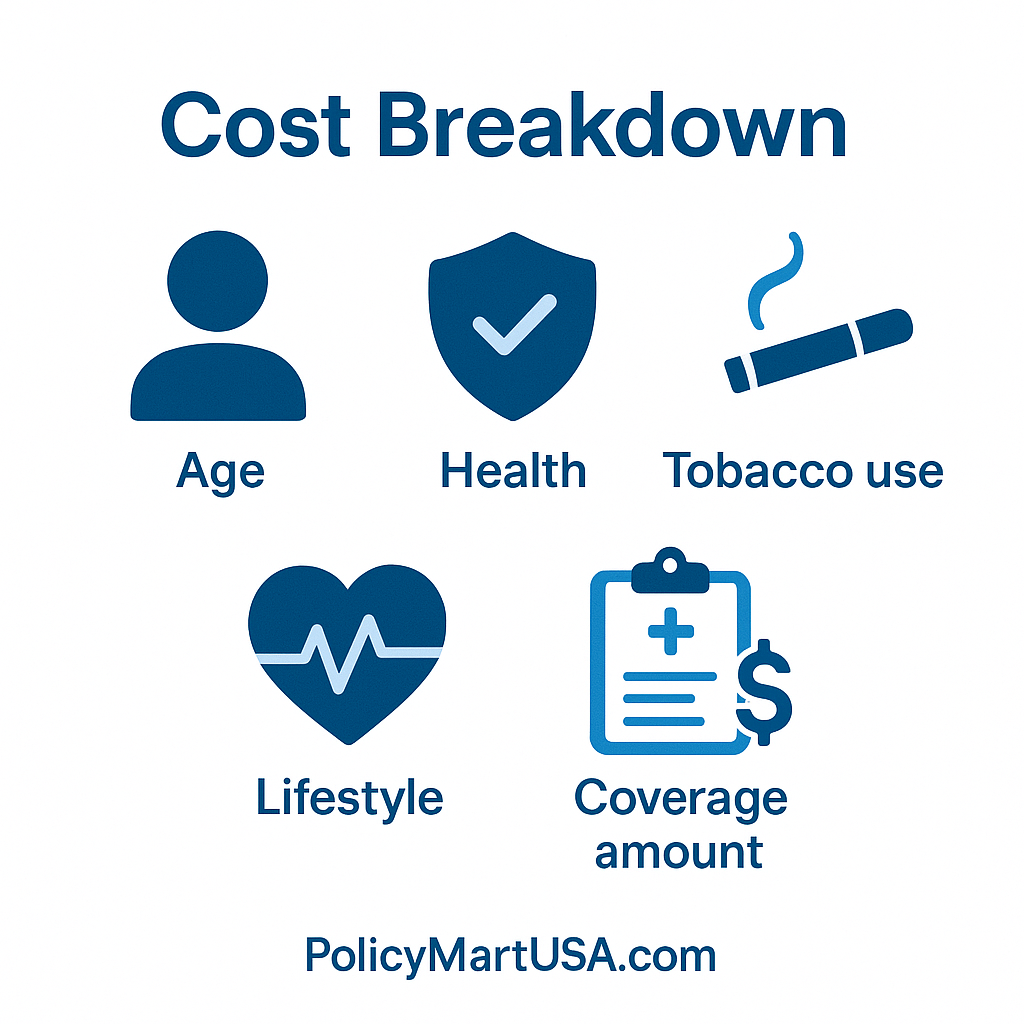

How Much Does Life Insurance Cost?

Competitor analyses show that term life rates vary significantly.

Average Monthly Life Insurance Rates

20-year, $1 million term policy:

- Healthy 35-year-old female: approx. $25–$65/month

- Healthy 35-year-old male: approx. $33–$85/month

What Affects Your Life Insurance Rates?

- Age

- Gender

- Health conditions

- Tobacco use

- Lifestyle & occupation

- Policy type and term length

- Coverage amount

Younger and healthier buyers always pay less. Rates increase with age and risk factors.

Life Insurance Policy Coverages (What’s Included?)

Life insurance coverages vary, but typically include:

Core Coverages

- Death benefit payout

- Terminal illness accelerated benefit

- Optional riders (child rider, waiver of premium, accidental death, etc.)

Optional Add-Ons

- Critical illness

- Disability income

- Return-of-premium rider

- Long-term care riders

Internal link suggestions:

- Explore related protections → Personal Insurance

- Compare health plans → Health Insurance

- Check auto coverage bundles → Auto Insurance

Comparison Table — Life Insurance Types

| Feature | Term Life | Whole Life | Universal Life |

|---|---|---|---|

| Coverage Length | 10–30 years | Lifetime | Lifetime |

| Cash Value | No | Yes | Yes |

| Flexibility | Low | Low | High |

| Rates | Cheapest | Higher | Varies |

| Best For | Families, budgets | Estate planning | Long-term flexibility |

How Much Life Insurance Do You Need?

Most experts recommend a death benefit of:

10–15× your annual income, plus:

- Mortgage balance

- Education costs

- Debt

- Future financial obligations

You can also use a life insurance calculator to refine your amount.

How to File a Life Insurance Claim

Life insurance claims are straightforward.

Step-by-Step Claims Process

- Contact the insurance company

- Submit the death certificate

- Provide beneficiary details

- Insurer reviews documents

- Payout is issued (usually within 1–4 weeks)

Life insurance claims are generally faster than homeowners or auto insurance claims.

Top Life Insurance Companies in the U.S.

- MassMutual – Strong financial strength, wide policy choices

- Nationwide – Great for affordable premiums

- Protective – Flexible term and universal options

- State Farm – Trusted nationwide network

- USAA – Best for military families

- Mutual of Omaha – Strong whole life options

- Progressive (via eFinancial) – Fast approvals, no-exam options

When Should You Buy Life Insurance?

Life insurance is cheapest when you’re:

- Younger

- Healthier

- Free of major medical conditions

Many people buy insurance during key life events:

- Marriage

- Buying a home

- Having children

- Starting a business

Is Life Insurance Worth It?

Yes — for anyone with dependents, debts, or long-term financial obligations, life insurance is one of the most reliable ways to protect family stability.

FAQ :

1. Why is term life insurance so cheap?

Term life doesn’t build cash value and only covers a fixed period, making it the most affordable option.

2. Which company is a legit life insurance provider?

Most large U.S. insurers like State Farm, Nationwide, USAA, Progressive, and MassMutual are reputable and highly rated.

3. How do I contact a life insurance company?

Every insurer lists contact details on their website, typically including phone, email, and mobile app support.

4. How do I cancel a life insurance policy?

You can cancel by contacting your insurer, submitting a written request, or stopping payments on term policies.

5. What does life insurance cover?

It covers a tax-free death benefit and, depending on the policy type, may include riders for illness, disability, or long-term care.

6. How much life insurance do I need?

Most families choose 10–15× their annual income, plus debt and mortgage considerations.