Know how disability insurance works, what it covers, typical rates, and how to choose the right policy to protect your income in the US.

Key Takeaways (Read This First)

- Disability insurance is a personal insurance policy that replaces part of your income if illness or injury keeps you from working.

- There are different disability insurance types (short-term, long-term, group, private, government) with very different rules and benefit periods.

- Typical disability insurance rates are often a small percentage of your income, but prices vary by state, provider, and age.

- Understanding what disability insurance coverages include (and exclude) is critical before you buy.

- Keep reading to learn how to compare disability insurance policies, file claims, and decide if personal insurance is worth it for your situation.

Disability Insurance: How It Protects Your Income When Life Goes Off-Track

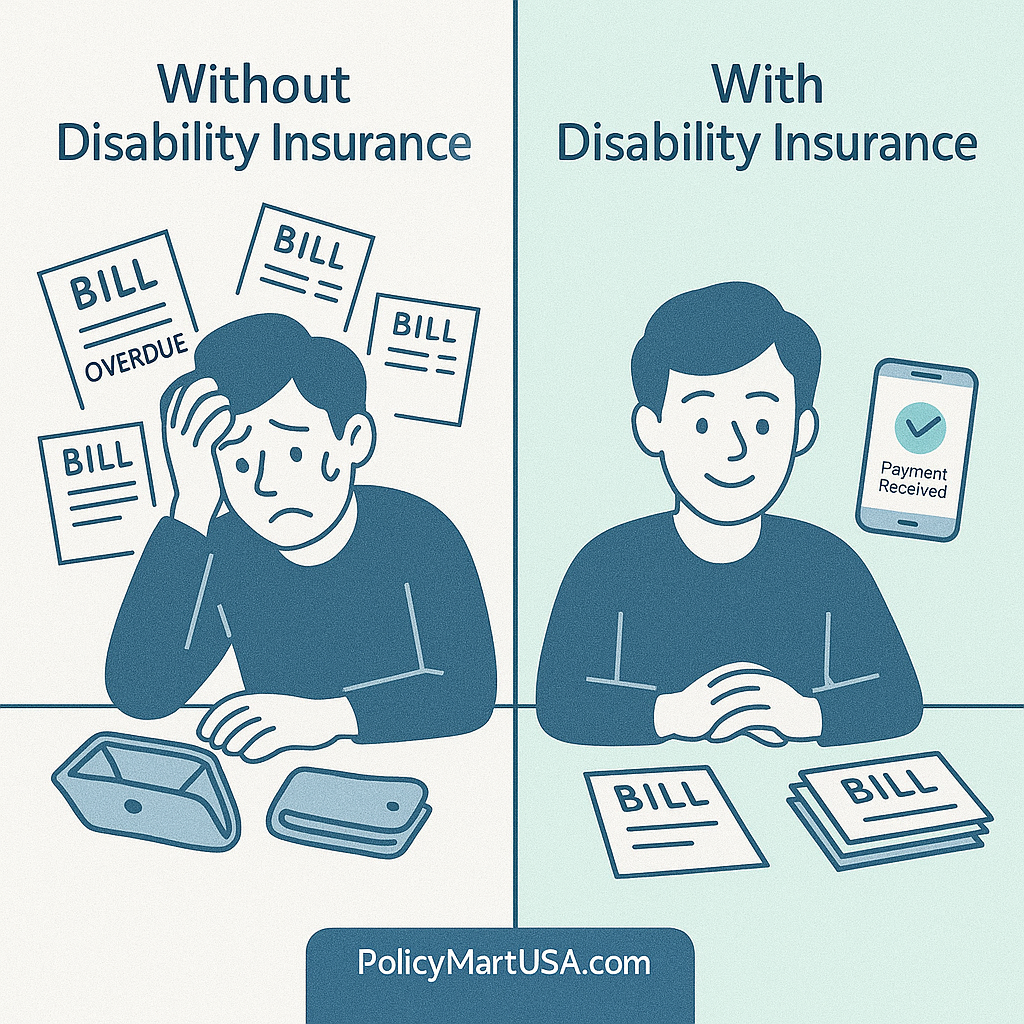

Most people insure their car and home—but forget to insure the one asset that pays for everything else: their ability to earn an income.

That’s where disability insurance comes in. If a serious illness, injury, or complicated pregnancy keeps you out of work, the right disability insurance policies can replace part of your paycheck so you can focus on recovery instead of worrying about bills.

In this guide from PolicyMartUSA.com, we’ll break down how disability insurance works in simple language, the main policy types, typical rates, and how to decide if it’s right for you.

Disclaimer: This article is for educational purposes only. It is not financial, tax, or legal advice. Prices vary by state, provider, and age.

What Is Disability Insurance?

Disability insurance is a type of personal insurance that pays you a monthly benefit if you can’t work due to a covered illness, injury, or medical condition.

- It usually replaces 50–70% of your income, depending on the plan.

- Benefits start after a waiting period (called the elimination period).

- Payments continue until you can work again or until the end of your benefit period (for example, 2 years, 5 years, or up to retirement age).

In other words: while health insurance pays doctors and hospitals, disability insurance pays you so you can cover rent, groceries, loan EMIs, childcare, and other daily expenses.

Main Disability Insurance Types

Understanding disability insurance types is the first step to choosing the right protection. The main categories are:

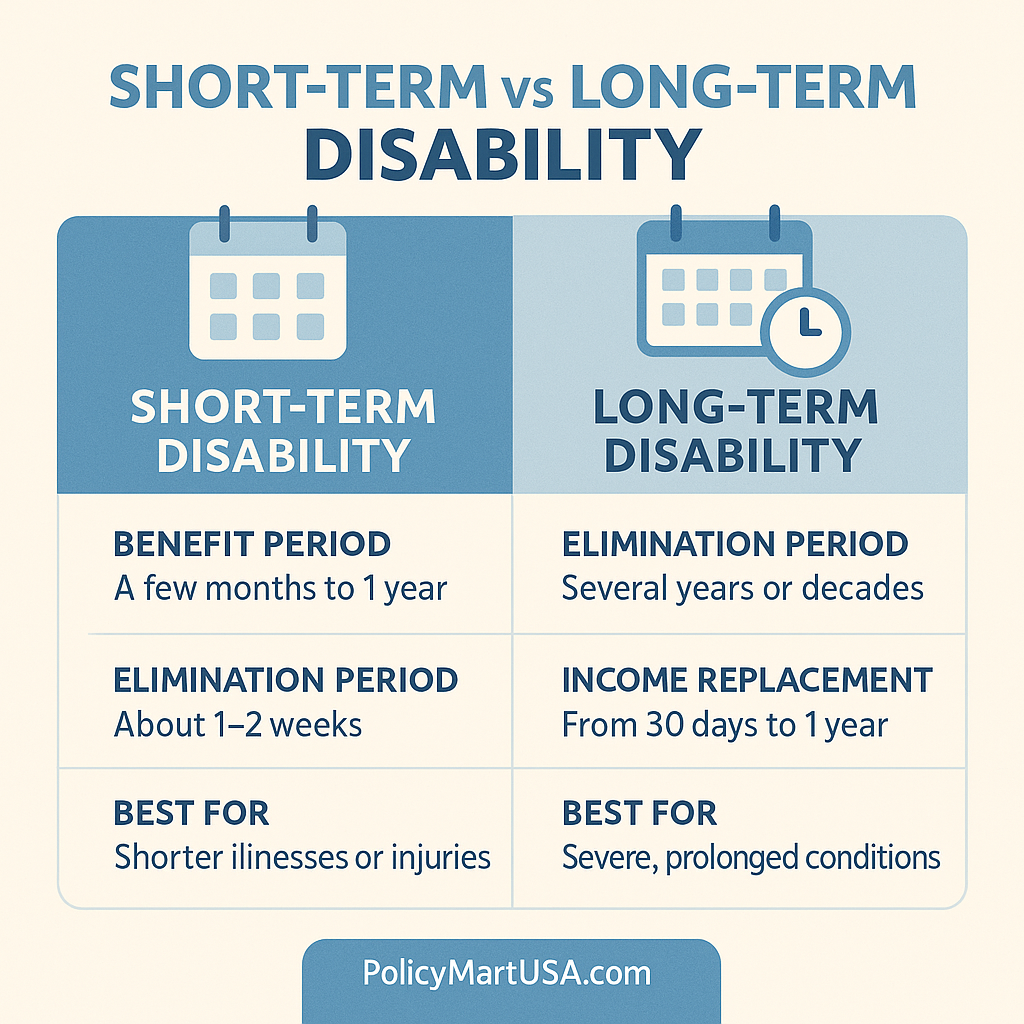

1. Short-Term Disability Insurance (STD)

These disability insurance policies are designed for shorter health events, like:

- Complicated pregnancy

- Minor surgery with a few months’ recovery

- Non-work accidents or illnesses

Key features:

- Benefit period: usually 3–6 months

- Elimination period: often under 2 weeks

- Benefit: can replace a high percentage of income (sometimes close to 100% of base salary, depending on the policy)

2. Long-Term Disability Insurance (LTD)

Long-term disability insurance kicks in when your health condition keeps you out of work for a longer time.

Typical features:

- Benefit period: several years, or up to age 65 or 67

- Elimination period: typically 3–6 months

- Benefit: often 50–70% of your income

These disability insurance coverages are important for serious injuries, chronic conditions, or illnesses like cancer, major back injuries, or neurological conditions.

3. Group Disability Insurance (Through Your Employer)

Many employers offer group disability coverage as part of the benefits package.

Pros:

- Often cheaper than buying individually

- Sometimes no medical exam

- Easy payroll deduction

Cons:

- Coverage may only replace part of your income

- Benefits may not cover bonuses or commissions

- You might lose coverage if you change jobs

4. Individual (Private) Disability Insurance

You buy these policies directly from an insurance company or agent.

Pros:

- You can customize the benefit amount, benefit period, and riders

- Policy can stay with you even if you switch jobs

- You may get a more favorable definition of “disability”

Cons:

- Medical underwriting is usually required

- Premiums can be higher than group plans

5. Government Disability Programs

Examples include:

- Social Security Disability Insurance (SSDI)

- Certain state disability programs

- Veterans disability benefits

These programs are valuable but usually have strict eligibility rules, waiting periods, and benefit limits. They’re not a full replacement for personal disability insurance for most families.

What Do Disability Insurance Policies Cover?

Disability insurance coverages vary by provider, but commonly include:

- Income loss due to illness (for example, cancer, heart disease, severe depression)

- Income loss due to injury (car accidents, falls, sports injuries, etc.)

- Complications related to pregnancy (depending on the policy)

Some policies use:

- Own-occupation definition: You’re considered disabled if you can’t perform the duties of your own job.

- Any-occupation definition: You’re only considered disabled if you can’t work in any reasonable job, not just your current role.

Own-occupation is usually more flexible but may cost more.

How Much Does Disability Insurance Cost?

Many people wonder, “How much is personal insurance like disability coverage?”

There’s no single number, but disability insurance rates are often a small percentage of your annual income. Your premium depends on:

- Age and gender

- Health and medical history

- Occupation (higher risk jobs usually pay more)

- Monthly benefit amount

- Length of the benefit period

- Elimination period (shorter wait = higher cost)

- Extra riders (cost-of-living adjustment, partial disability, future increase options, etc.)

Because of all these factors, one person might pay $30–$50 per month, while another may pay much more for higher coverage.

Again: Prices vary by state, provider, and age.

Get Your Free Insurance Quote

Comparison Table: Short-Term vs Long-Term Disability Insurance

| Feature | Short-Term Disability (STD) | Long-Term Disability (LTD) |

|---|---|---|

| Main purpose | Temporary income replacement | Long-term / serious disability |

| Typical benefit period | 3–6 months | Several years or to retirement age |

| Elimination period (waiting) | A few days to 2 weeks | 3–6 months |

| % of income replaced | Up to 100% (varies by policy) | ~50–70% (varies by policy) |

| Commonly offered through | Employers (group policies) | Employers & private insurers |

| Best for | Short recoveries, pregnancies | Major injuries & chronic illnesses |

Use this table as a quick guide when you compare disability insurance policies online or with an agent.

Is Personal Insurance Like Disability Coverage Worth It?

You might be asking: “Is personal insurance worth it if I’m healthy right now?”

Consider:

- Many disabilities are caused by illness, not just dramatic accidents.

- Losing your income for even 6–12 months can disrupt long-term goals like buying a home, paying off debt, or funding your child’s education.

- According to multiple studies, a significant portion of workers will face a disability at some point in their careers, and many families would struggle within months without a paycheck.

For many households, disability insurance is a core part of a personal insurance plan, alongside health, auto, and life coverage.

While no policy can remove all risk, the right disability coverage can keep a tough season from becoming a full financial crisis.

How to File a Disability Insurance Claim (General Steps)

Each company has its own process, but the basics are similar. If you’re wondering how to file a personal insurance claim for disability, the general steps look like this:

- Notify your employer or insurer as soon as you know you’ll be out of work longer than a few days or weeks.

- Complete claim forms (you may have separate forms for you, your employer, and your doctor).

- Provide medical documentation that supports your disability and expected recovery time.

- Wait for claim review – some policies may request additional information.

- Receive benefits if approved, based on your elimination period and benefit amount.

Tip: Keep copies of all forms, emails, and letters. If you’re unsure, ask the insurer or HR department to walk you through the timeline.

Where Disability Insurance Fits in Your Overall Insurance Plan

Disability coverage doesn’t replace other policies—you’ll usually combine it with:

- Auto insurance for your car needs (learn more at

/auto-insurance/) - Health insurance to pay medical bills (see

/health-insurance/) - Personal insurance for other life risks like life insurance and umbrella policies (explore

/personal-insurance/)

Thinking in terms of a complete protection plan helps you avoid coverage gaps where a single event could shake your finances.

Example :

Imagine Alex, a 38-year-old nurse:

- She injures her back and can’t work for several months.

- Short-term disability pays 60% of her income while she starts treatment.

- If her recovery is slower than expected, her long-term disability policy can take over, continuing to pay a portion of her income while she adjusts or retrains for a different role.

Without disability insurance, Alex might need to drain savings, rely on credit cards, or borrow from family just to stay afloat.

FAQs: Disability Insurance & Personal Insurance Questions

1. Is personal insurance worth it if I already have savings?

Personal insurance, including disability insurance, is designed so you don’t need to drain your savings immediately when something goes wrong. Savings can run out quickly if you’re out of work for many months. For many people, combining an emergency fund with disability coverage provides stronger protection.

2. What does personal insurance cover when it includes disability benefits?

Personal insurance that includes disability benefits generally covers income loss when you can’t work due to a covered illness, injury, or medical condition. It doesn’t usually pay your medical bills—that’s what health insurance is for—but it helps replace part of your paycheck so you can handle rent, utilities, food, and other daily expenses.

3. How much is personal insurance that includes disability coverage?

How much is personal insurance depends on factors like your age, health, occupation, benefit amount, and benefit period. Disability insurance rates can be higher for physically demanding jobs or longer benefit periods. Getting quotes from multiple insurers is the best way to see your real price.

4. How do I know if an insurance company is legit?

If you’re wondering, “Is [company] legit?”, look for:

- Strong financial strength ratings from independent rating agencies

- A valid license to operate in your state

- Clear policy documents and claims information

- Helpful customer service and transparent online reviews

If you’re unsure, talk to a licensed insurance professional or check with your state’s insurance department.

5. How do I cancel a disability insurance policy if it no longer fits my needs?

Most companies allow you to cancel a disability policy by contacting customer service or your agent and submitting a written request. Before you cancel, consider whether you have another policy in place and how losing this coverage would affect your long-term financial plan.