Learn how auto insurance works, what it covers, average rates, claim process & tips to save. Compare top coverage types easily on PolicyMartUSA.com.

⭐ Key Takeaways

- Auto insurance protects you from financial loss after accidents, theft, or vehicle damage.

- Every state sets minimum liability requirements, but additional coverages can offer broader protection.

- Auto insurance rates depend on driving history, location, vehicle type, and coverage levels.

- Claim handling speed varies by provider; knowing the steps prevents delays.

- Comparing plans yearly may help you find better personal insurance rates.

Auto Insurance Guide 2026 — Coverage, Rates & How It Works

Auto insurance is one of the most essential personal insurance types in the United States. Whether you drive daily or occasionally, having the right policy protects you from unexpected financial stress caused by accidents, theft, natural disasters, or injuries.

In this guide, we break down auto insurance policies, personal insurance coverages, personal insurance rates, and how personal insurance claims work—all in a simple, easy-to-read format designed for U.S. drivers.

What Is Auto Insurance & Why Does It Matter

Auto insurance is a contract between you and your insurer. You pay a monthly or annual premium, and in return, the insurer covers certain losses if something happens to your vehicle or if you cause damage to others.

Auto insurance falls under the broader category of personal insurance policies—coverage designed to protect your income, assets, and financial security.

What Auto Insurance Typically Covers

Most policies include:

- Vehicle damages (your car & others’)

- Bodily injuries caused to others

- Medical expenses after an accident

- Theft or vandalism losses

- Property damage

Disclaimer: Prices vary by state, provider, and age.

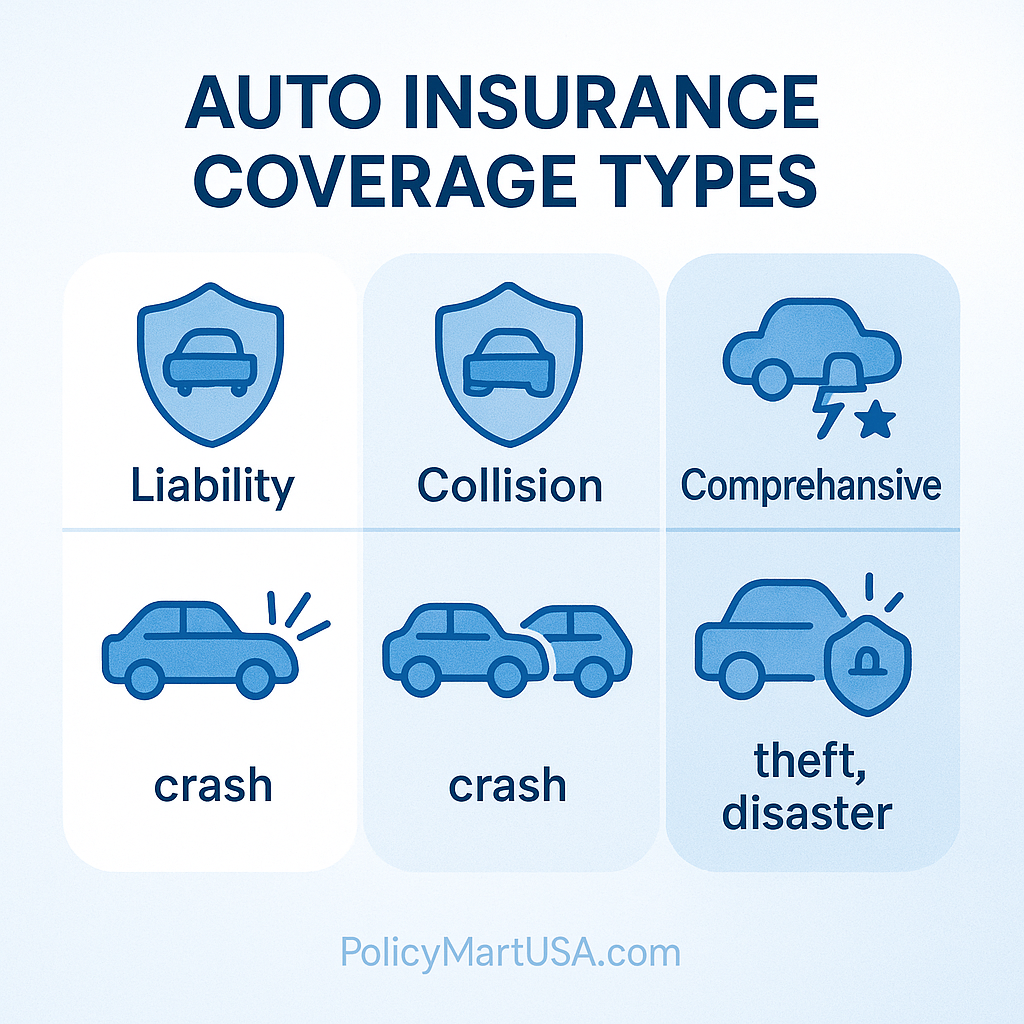

Types of Auto Insurance Coverages

Understanding personal insurance coverages within auto insurance helps you decide what you truly need.

Liability Coverage (Legally Required in Most States)

Covers:

- Bodily injuries you cause

- Property damage you cause

This is the most basic requirement in almost every state.

Collision Coverage

Pays for repairs to your car after a collision—regardless of fault.

Comprehensive Coverage

Protects your vehicle from non-collision events such as:

- Theft

- Fire

- Vandalism

- Natural disasters

- Falling objects

Uninsured / Underinsured Motorist (UM/UIM)

Covers your injuries or vehicle damage when the other driver:

- Has no insurance

- Has insufficient insurance

Many states require this coverage due to rising uninsured driver rates.

Personal Injury Protection (PIP) or Medical Payments (MedPay)

Covers:

- Medical bills

- Lost wages

- Funeral costs

This applies regardless of who caused the accident.

Gap Insurance

If your car is totaled, gap insurance pays the difference between:

- Your loan balance

- Your vehicle’s actual market value

Ideal for new cars or vehicles that depreciate quickly.

Comparison Table — Auto Insurance Coverages

| Coverage Type | What It Covers | Required? |

|---|---|---|

| Liability | Injuries & property you cause | Mandatory in most states |

| Collision | Your car after a crash | Optional |

| Comprehensive | Non-collision damage | Optional |

| UM/UIM | Accidents with uninsured drivers | Required in some states |

| PIP/MedPay | Medical bills & lost income | Required in select states |

| Gap Insurance | Loan vs. car value difference | Optional |

How Much Does Auto Insurance Cost?

Auto insurance pricing—also known as personal insurance rates—varies widely based on:

Factors That Affect Your Rates

- Driving history (accidents, tickets)

- Age & gender

- State & ZIP code

- Vehicle make/model/year

- Credit score (in most states)

- Coverage limits chosen

- Annual mileage

Drivers with clean records usually pay significantly less.

Average Rates

- Minimum liability: $600–$1,200 per year

- Full coverage: $1,600–$2,800 per year

(Disclaimer: Prices vary by state, provider, and age.)

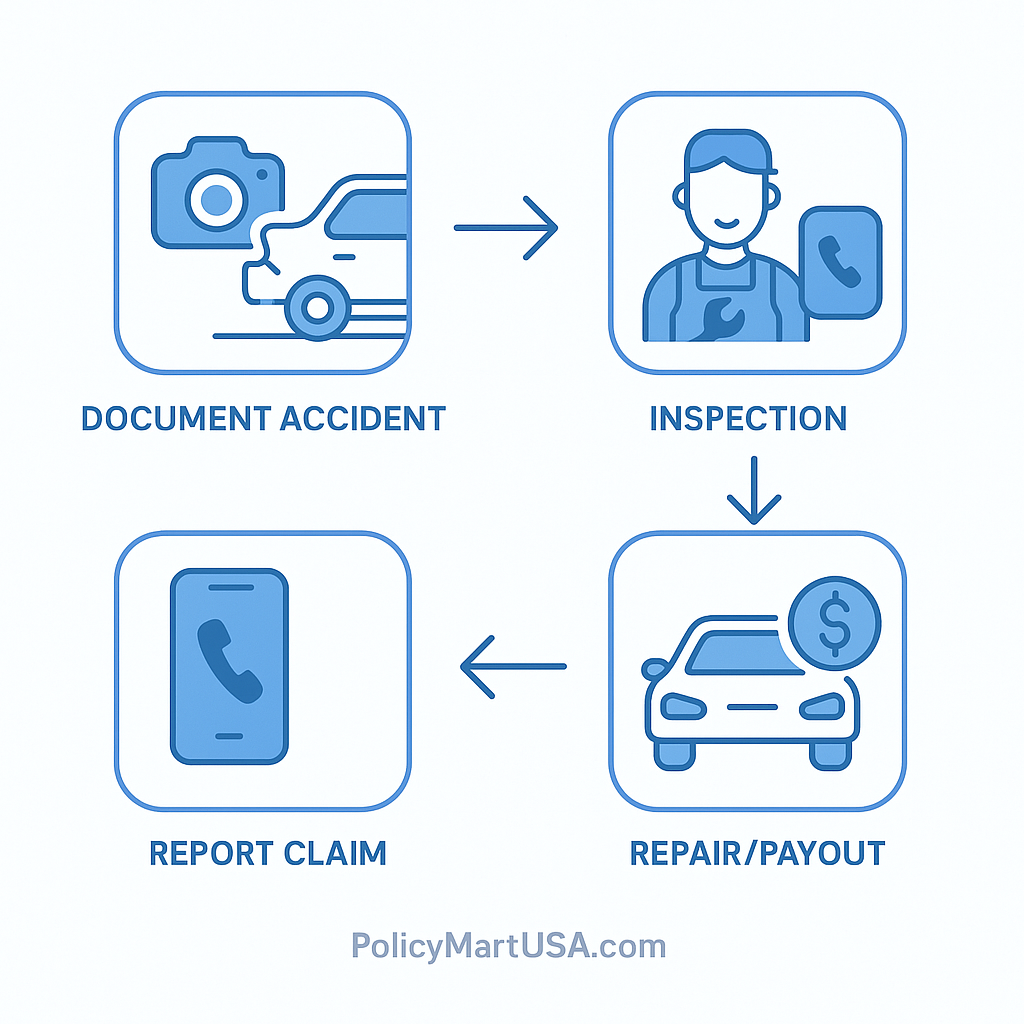

How Auto Insurance Claims Work

Filing personal insurance claims after an accident is straightforward if you know the steps.

H3: Steps to File a Claim

- Ensure safety and seek medical care if needed.

- Document the scene with photos & notes.

- Exchange information with all parties.

- Report the incident to your insurer immediately.

- Provide documentation (police report, images, bills).

- Get a repair estimate or inspection.

- Receive payout or get repairs done at a preferred shop.

How long does it take?

Simple claims may resolve in a few days; complex cases can take several weeks.

How to Choose the Right Auto Insurance Policy

Assess Your Needs

Consider:

- Value of your vehicle

- Whether you drive daily or occasionally

- Your financial ability to pay deductibles

- The level of risk in your city/state

Compare Multiple Quotes

Don’t rely on a single company.

Every insurer has different formulas and discounts.

Check Company Reputation

Look at:

- Customer reviews

- Claim satisfaction score

- Financial stability ratings (A.M. Best, Moody’s)

Use Discounts:-

Common discounts include:

- Safe driver

- Bundling home + auto

- Military or senior discounts

- Defensive driving courses

- Low-mileage usage-based programs

Future Trends in Auto Insurance:-

Telematics & Usage-Based Insurance

Programs like Progressive Snapshot or Allstate Drivewise adjust your rate based on driving habits.

Electric Vehicles & Battery Costs

EV insurance rates vary due to specialized repair requirements.

Autonomous Vehicles Impact

Liability may gradually shift from drivers to manufacturers—transforming insurance structures.

Frequently Asked Questions:-

1. Why is some auto insurance so cheap?

Usually due to:

- Minimum coverage

- High deductibles

- Limited features

- Usage-based discounts

2. Are insurance companies legit?

Most major U.S. insurers (State Farm, Progressive, GEICO, Allstate, USAA) are reputable and licensed nationwide.

3. How do I contact my insurance provider?

Check:

- Your insurance card

- Mobile app

- Official website contact page

4. How to cancel an auto insurance policy?

Typically requires:

- Calling your insurer

- Signing a cancellation form

- Providing proof of new coverage (in some states)

5. What does auto insurance cover?

Covers injuries, vehicle damage, property damage, theft, and accident-related medical costs—depending on your chosen coverages.

6. How much is auto insurance?

Depends on driving history, state, vehicle, and coverage level. Costs range widely across the U.S.

Final Thoughts

Auto insurance is one of the most critical personal insurance policies for protecting your finances, vehicle, and loved ones. Whether you’re seeking basic liability coverage or full protection, comparing the right coverages—and reviewing your policy annually—ensures you stay prepared for unexpected events.